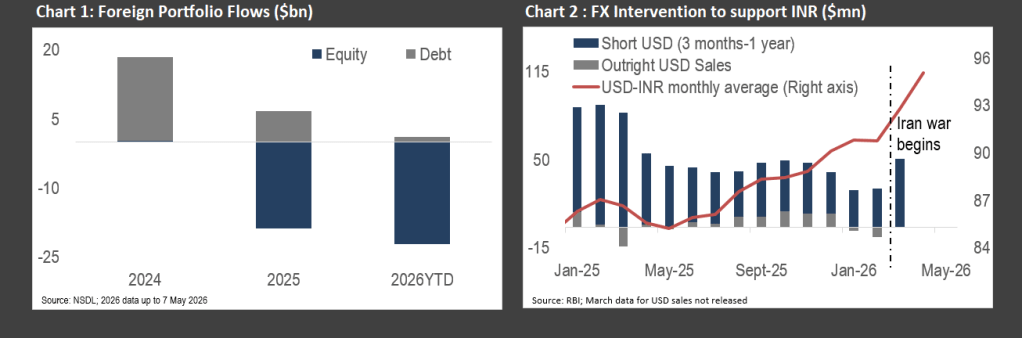

The rupee has been under sustained pressure for a while now. Having weakened by 5% over 2025 due to record foreign portfolio outflows, it has further depreciated by 5.2% so far in 2026. Cumulative foreign portfolio outflows since 2025 have topped $40 billion with half of it happening in the two months since start of the Iran conflict. The steady deterioration in the value of the rupee has compelled the RBI to repeatedly intervene in the FX market. See Charts 1 and 2.

In 2025, the RBI sold $52 billion in the spot market while simultaneously building a sizable short dollar position in the forwards market. The outstanding short dollar position peaked at $89 billion in February 2025 (with maturities of under one year). Between March 2025 and January 2026, the RBI allowed these positions to unwind to a low of $28bn as falling oil prices eased dollar demand for financing oil imports and kept the rupee supported despite portfolio outflows.

The RBI briefly turned a net buyer of dollars in 2026, purchasing $10 billion in the spot market during January and February. That window closed abruptly with the beginning of the Iran war. By end-March, the RBI had rebuilt a $50 billion short dollar position in the forwards market, concentrated in maturities of three months to one year — signaling a clear intent to provide near-term support to the currency. Additional restrictions on the offshore positions of domestic banks were imposed in March and April to squeeze out speculative positions that had been amplifying downward pressure.

The heavy use of non deliverable forwards (NDF) has allowed the RBI to avoid a sharp decline in headline foreign exchange reserves, which stood at $699 billion as of 24 April 2026 — equivalent to nearly 11 months of import cover.

Traditionally, foreign capital flows and oil import costs have been two dominant sources of pressure on the rupee. When both deteriorate simultaneously, as has happened since March 2026, the strain from dollar outflows directly affects currency reserves and weakens the rupee. Persistent foreign portfolio outflows combined with rising oil import costs have reduced India’s foreign currency assets to $555 billion by April 2026, a $62 billion decline from the all-time peak reached in September 2024. The rupee hit an all time low of 95.39 per dollar on May 5.

While data for the RBI’s NDF position over April and May isn’t available yet, it is likely to have increased further. Yet these large forward positions and other measures have not prevented the rupee from breaching the 95 per dollar mark. In fact, the frequently occurring maturity of these short term positions creates a third source of dollar demand in the spot market, bringing further pressure on the currency.

Another key side effect of these maturing NDF positions is the recurring drain on rupee liquidity.

A Structural Problem in Domestic Liquidity

This brings us to a fundamental problem. The Indian banking system has been facing recurring liquidity deficits over the past five years, reflecting a structural deterioration in deposit mobilisation. Household savings have migrated steadily away from bank deposits towards mutual funds and equities, eroding the low-cost funding base that banks relied on. Meanwhile, regulatory constraints on bond issuance by banks have limited their ability to replace that funding from capital markets. The credit-deposit ratio — the clearest barometer of this imbalance — hit a peak of 83% in mid-March 2026, a level that severely constrains the headroom for further credit expansion.

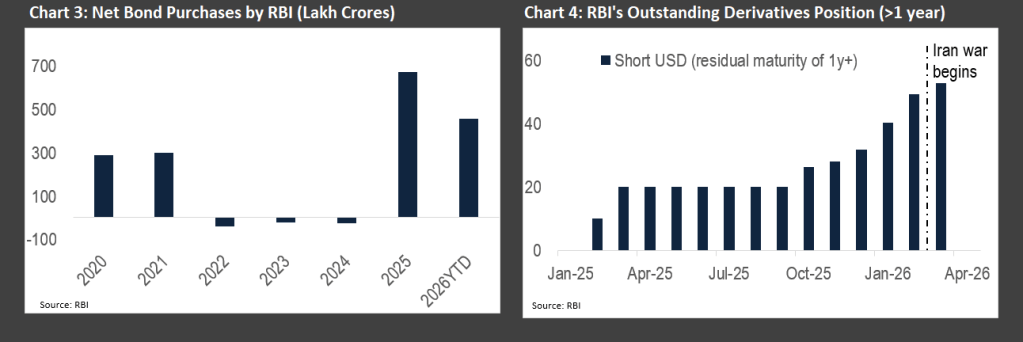

Historically, the RBI intervened during seasonal or temporary liquidity shortages, such as those associated with tax outflows or festival-related cash demand. Since 2025, however, the higher frequency of FX intervention has emerged as an additional drain on liquidity, transforming bond purchases from a discretionary support tool into a recurring necessity. This has increased the RBI’s net purchases of government bonds. See Chart 3.

Alongside bond purchases, the RBI has also relied on 3-year dollar-rupee swaps as a tool to simultaneously sterilise its FX intervention and inject durable rupee liquidity. Under this arrangement banks sell dollars to the RBI and agree to buy them back at a predetermined rate after three years. The appeal is clear. Reserves rise, rupee liquidity is injected and the transaction does not disturb the government bond market. Consequently, the RBI’s outstanding short dollar position in maturities beyond one year rose from $10 billion in February 2025 to $53 billion by March 2026. See Chart 4.

Despite these infusions, the hard won liquidity surplus of the banking system seems fragile. Cash withdrawals rose by 12% during the first half of April 2026, the highest since the 2016 demonetization, and extended a six-month trend. This adds to the liquidity absorbing effects of elevated oil import costs, capital outflows and FX intervention, weakening banks’ liquidity buffers and constraining their ability to lend.

The Hidden Costs of Sterilizing FX Intervention

While the RBI cannot influence oil import costs or portfolio flows, it can can sterilize its FX intervention by bond purchases. But this approach carries its own distortions. The central bank already holds 14% of outstanding government securities as of end-2025 and absorbed 82% of the government’s net bond supply in FY26. Having such a large captive buyer of government bonds nudges yields higher and raises borrowing costs for the private sector.

If it chooses to sterilize by conducting more swaps, it creates a looming dollar demand over the next three years. As the short dollar leg of these swaps matures, the RBI would need to buy dollars in the spot market to close out its position. In an environment where the rupee faces structural downward pressure from a largely inelastic demand for oil imports and portfolio outflows, this creates a predictable ceiling on any sustained currency recovery. Markets will price in the future dollar demand even before the swaps mature.

The deeper issue is that INR valuation and domestic credit rely on the same limited pool of rupee liquidity. Tighter liquidity supports the rupee temporarily but hinders credit growth and vice versa. The best hope for India is for portfolio flows to recover materially or for oil prices to provide sustained relief. At present, neither appears especially likely.

Related Reading

Rupee gains sharply as oil slides, NDF dollar selling gathers pace

Rupee sinks to fresh closing low of 95.08 against USD on NDF maturities, firm crude

Indian banking’s held back by inadequacy of long-term funding

India’s Banking Liquidity Paradox: Massive infusion but hardening yields